Builders Prepare for 85% Insurance Premium Surge in 2025

Picture inspecting a newly framed structure, with the scent of fresh lumber filling the air, yet recognizing that insuring the subsequent project could nearly double in expense. Builders encounter this scenario as premiums escalate rapidly. Such a rise resembles an abrupt financial challenge amid constrained budgets. Past experiences with modest liability increases prompted reevaluations of schedules and resources, but an 85 percent escalation alters the landscape fundamentally.

The Challenge Dominating Builder Discussions

The construction industry operates on narrow profit margins. Fluctuating material prices, workforce gaps, and regulatory delays already demand careful management. Projected insurance rate increases amplify these pressures, prompting contractors, project leaders, and solo operators to question project viability.

This premium escalation impacts beyond major firms. Small-scale operations, such as family-run enterprises or regional teams, experience the most immediate effects. It reshapes bidding processes, cost estimates, and hazard evaluations. Key drivers include elevated claim settlements, rigorous policy evaluations, and inflated expenses for materials and post-incident repairs.

Elevated liability insurance costs permeate all aspects of operations. Builders must adjust job pricing, client selection, and onsite safety implementations accordingly.

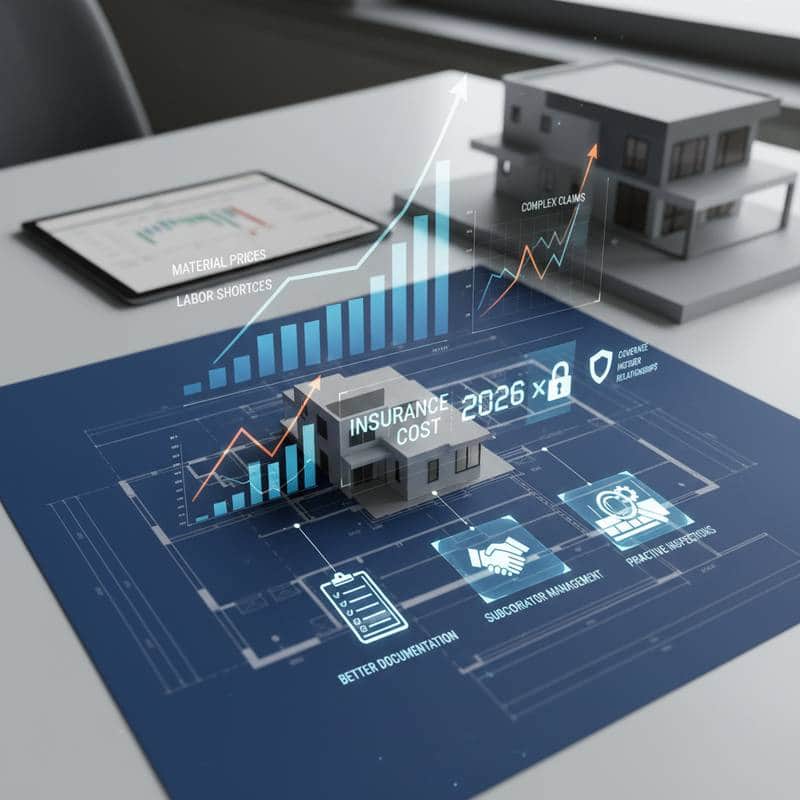

Factors Fueling the Sharp Premium Increases

Insurers respond to a surge in substantial, intricate claims within construction. Incidents tied to severe weather, workplace mishaps, and logistical disruptions contribute to these trends. Providers implement stricter terms, incorporate limitations, and elevate deductibles to curb their exposure, resulting in higher costs and reduced protection for policyholders.

A single minor incident, such as water damage swiftly resolved, once led to a one-third premium hike upon renewal. When such events multiply across the sector, insurers reassess overall risk profiles. This adjustment manifests as the anticipated 85 percent increase that builders now anticipate.

Initial Steps for Premium Management

Approach insurance selection with the same diligence applied to material sourcing. Compare multiple providers before committing, just as with any essential supply. Consider these targeted areas for improvement:

-

Compare Providers Thoroughly

Providers vary in risk assessment approaches. Those focused on construction may extend advantageous terms to entities with unblemished safety histories or robust project oversight frameworks. -

Minimize Site Hazards

Each prevented claim preserves funds. Conduct regular safety inspections, enforce protective equipment usage, and maintain comprehensive records. Documenting safety installations through photographs aids compliance checks and policy renewals. -

Consolidate Coverage Options

Integrating general liability, builder's risk, and property insurance with a single provider often yields savings. This consolidation streamlines administrative tasks, crucial for overseeing diverse projects. -

Examine Subcontractor Contracts

Verify that subcontractors maintain independent coverage. Contracts should delineate responsibilities clearly to shield against liability for others' oversights. -

Adjust Deductibles Strategically

Opting for higher deductibles lowers premiums, provided sufficient reserves cover minor incidents. Evaluate the trade-offs through detailed calculations.

Quantifying the Financial Impact

Builders frequently inquire about tangible cost implications. Premiums differ by operation scale, but a mid-sized contractor's annual expense could escalate by thousands. These additions strain yearly budgets, necessitating absorption or client pass-throughs. For modest firms, such increments can tip jobs from profitable to deficit.

Residential work carries distinct risk profiles compared to commercial endeavors, warranting tailored quotes. Regional providers or specialized brokers may deliver competitive rates over national options. Engage builder associations or professional networks for recommendations. A local broker's onsite evaluation once facilitated a more equitable premium based on operational insights.

Integrating Risk Reduction into Design

Underwriters scrutinize risk management practices, extending to material and technique selections. Choices that lower exposure include:

- Fire-retardant materials to diminish property damage potential.

- Non-slip surfaces in busy zones to curb injury incidents.

- Adequate airflow systems and dampness controls to avert mold disputes and associated litigation.

Incorporating enhanced fire-rated engineered wood in one project registered positively with the insurer. While not drastically reducing costs, it moderated subsequent increases.

Broader Implications for Clients and Timelines

Premium surges extend beyond internal finances. Clients encounter elevated estimates, postponed initiations, or modified payment terms. Developers, investors, and homeowners observe extended discussions as builders recalibrate figures. Clear communication regarding insurance influences fosters credibility and demonstrates prudent management.

Scheduling adjustments emerge as well. Some builders extend intervals between projects to stabilize cash flow or await clearer premium details. Others incorporate expanded contingency funds in agreements to buffer against volatility.

Regional Tactics for Cost Control

In regions with robust trade organizations or builder collectives, collaboration proves invaluable. Shared insights mitigate individual burdens. Certain areas offer collective insurance arrangements for certified professionals, stabilizing rates.

Consult local builder federation chapters for insurer affiliations attuned to regional codes, climates, and project varieties. These alliances yield cost-effective protection, particularly for safety-compliant operations.

Time policy evaluations post-key achievements rather than solely at renewal. Updating providers on finished works, upgraded safety protocols, or fresh credentials influences rate determinations.

Sustaining Viability Amid Elevated Premiums

Builders must address this evolution directly. Insurance remains a core outlay, and neglect exacerbates future pressures. Implement stringent financial oversight in project planning. Embed insurance expenses in estimates explicitly. Monitor claim records meticulously and prioritize preventive measures. Incremental enhancements, such as improved illumination for evening tasks or routine machinery inspections, yield long-term returns.

Strengthening Operations Against Market Shifts

By embedding these practices, builders fortify resilience. Proactive risk handling not only tempers immediate costs but also enhances overall project reliability. This approach ensures sustained competitiveness in an unpredictable sector.