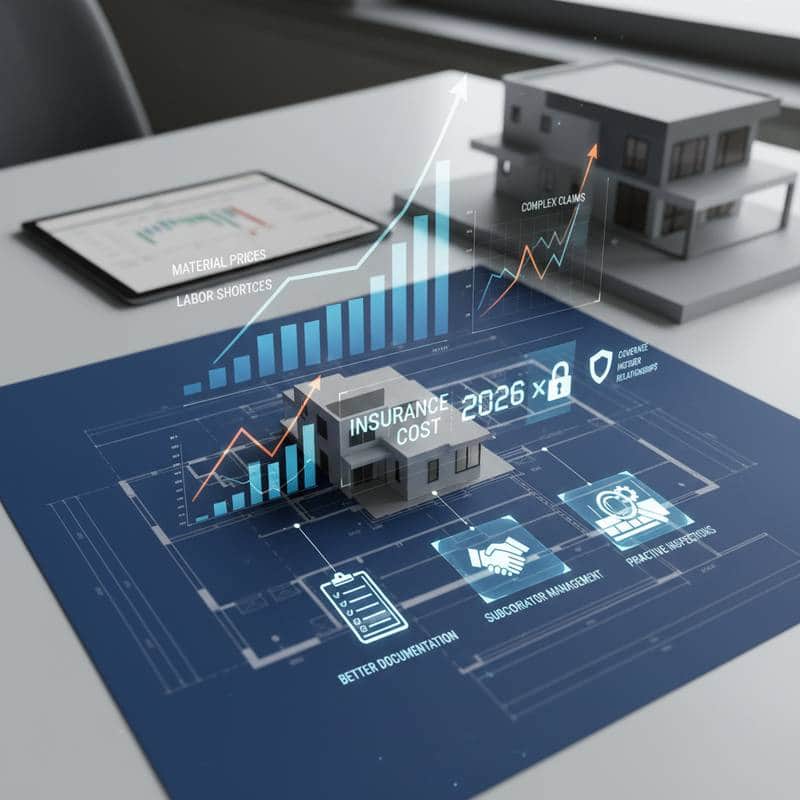

Builders Prepare for 85% Insurance Premium Increases in 2025

Recent renewal quotes reveal a stark reality for construction firms: insurance premiums may escalate by up to 85% in 2025. Seasoned contractors report these figures prompt immediate reviews of financial projections and operational strategies. Such shifts compel the industry to address underlying vulnerabilities while seeking sustainable solutions.

Factors Driving the Sharp Rise in Insurance Rates

Several interconnected elements contribute to this escalation. Insurers cover risks including general liability, worker injuries, natural disasters, and material defects. Recent years have seen increased claims from severe weather events, supply chain disruptions, and volatile material pricing, which strain insurer resources.

To maintain solvency, insurers adjust premiums upward. Even routine projects now appear more hazardous in actuarial assessments. Small-scale residential contractors experience comparable pressures, underscoring the widespread impact on the sector.

Impacts on Daily Construction Operations

Premium hikes extend beyond profit margins to influence project planning and pricing. Insurance represents a critical yet often overlooked expense that affects labor allocation and material selections. A sudden 85% increase alters cost structures fundamentally.

Contractors respond by incorporating elevated insurance expenses into bid calculations. Some delay business expansions or new hires to control overhead. Collaborative approaches, such as shared insurance among multiple firms, emerge as viable methods to distribute costs more evenly.

Key Insurance Types Experiencing the Greatest Increases

Construction operations typically require a portfolio of essential coverages:

- General liability insurance, which safeguards against claims of property damage or bodily injury.

- Builder’s risk insurance, protecting materials and ongoing structures from loss.

- Workers’ compensation, providing support for employee injuries or illnesses.

- Professional liability, addressing errors in design or project oversight.

- Commercial auto coverage, insuring vehicles and equipment used at job sites.

Builder’s risk and general liability policies face the most significant adjustments. These categories prove particularly vulnerable to claims involving extreme weather, site theft, vandalism, or operational accidents. High-cost incidents in these areas prompt insurers to recalibrate rates aggressively.

Strategies for Builders to Mitigate the Premium Surge

Proactive measures enable builders to navigate rising costs effectively. Early action focuses on optimization and risk reduction to preserve financial stability.

1. Evaluate and Adjust Coverage Levels.

Over-insurance often inflates expenses unnecessarily, particularly for modest projects. Engage an experienced insurance broker to analyze current policies and align protection with specific project exposures. Tailored adjustments can eliminate redundant elements without compromising security.

2. Enhance Site Safety Protocols and Record-Keeping.

Insurers reward demonstrable commitment to safety through favorable rating adjustments. Implement rigorous training programs, conduct regular equipment inspections, and document compliance with protective standards. These practices not only lower incident rates but also strengthen renewal negotiations.

3. Consolidate Policies for Efficiency.

Combining multiple coverages or projects with a single provider often unlocks volume-based discounts. Centralized management reduces administrative burdens, such as tracking varied renewal schedules. This streamlined approach supports long-term cost control.

4. Leverage Group or Association-Based Insurance Options.

Trade organizations frequently secure preferential rates through bulk negotiations. Review affiliations with local or national builder groups to access these programs. Participation provides competitive advantages without requiring individual market shopping.

5. Integrate Insurance Costs Transparently into Project Bids.

Clear communication about industry-wide cost pressures builds client understanding. Detail how insurance factors into pricing during initial consultations. This transparency fosters stronger relationships and minimizes disputes over adjustments.

Implications for Homeowners and Project Clients

Individuals commissioning builds or renovations may notice indirect effects on overall costs. Builders compelled to absorb premium increases often reflect portions in client quotes or provide expanded expense breakdowns. Such adjustments ensure comprehensive protection remains in place.

Transparency in these discussions highlights a builder’s dedication to reliability. It reassures clients that coverage addresses potential disruptions, such as weather delays or supply setbacks. Well-insured projects proceed with fewer interruptions and greater accountability.

Opportunities Arising from Escalating Insurance Costs

This financial pressure catalyzes positive transformations in risk evaluation. Advanced tools like digital monitoring systems, aerial surveys via drones, and predictive weather modeling enable precise hazard assessments. Adoption of these technologies promises more equitable premium structures over time.

Enhanced collaboration between builders and clients also gains momentum. Shared awareness of cost dynamics encourages flexible scheduling and joint contingency planning. These developments contribute to more resilient operations amid economic challenges.

Strengthening Project Resilience Through Informed Risk Management

Effective navigation of insurance increases demands vigilance in policy reviews, contract scrutiny, and safety prioritization. Builders benefit from consulting specialists early and maintaining meticulous records. Clients support success by articulating needs clearly at the outset.

Ultimately, construction thrives on balancing innovation with precaution. Robust insurance frameworks underpin this process, allowing teams to deliver enduring structures despite unforeseen challenges. Prepared professionals turn potential obstacles into opportunities for refined practices.