Why Construction Insurance Rates Surged 45% in 2025

Construction projects form the backbone of economic growth, yet the costs associated with insuring them have risen sharply. In 2025, premiums for construction insurance have jumped by 45%, affecting everyone from large contractors to individual homeowners undertaking renovations. This surge stems from a combination of economic pressures, environmental challenges, and policy shifts that demand attention from the industry.

Understanding these drivers is essential for mitigating their impact. Builders must adapt their budgeting and risk management practices to maintain profitability. Homeowners, too, can take steps to secure favorable terms without compromising protection.

Key Drivers Behind the Premium Increase

Escalating Material Costs

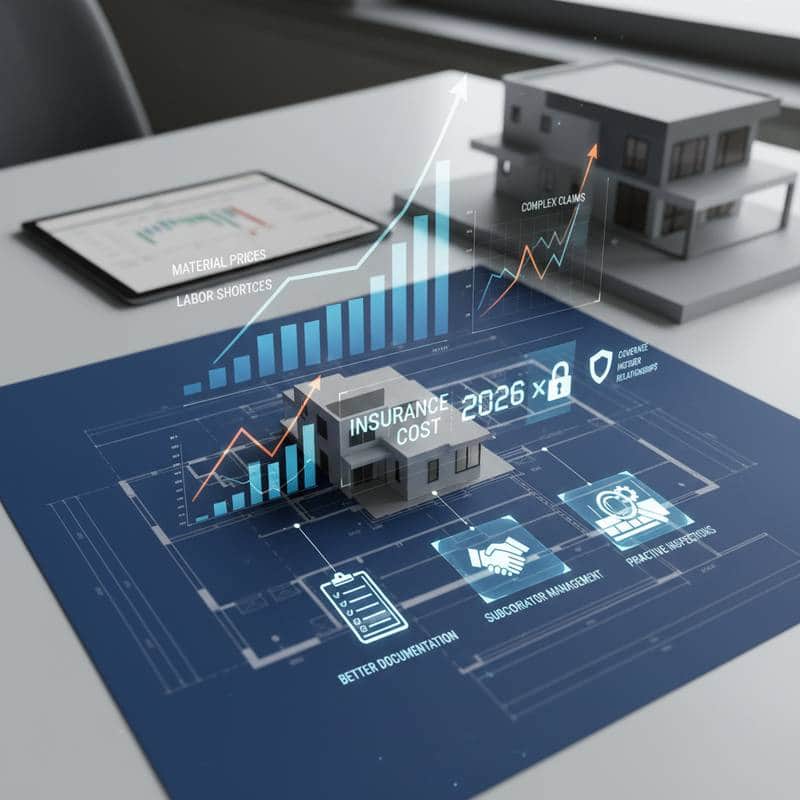

The price of construction materials has climbed steadily over recent years, influenced by global supply chain disruptions and inflationary trends. Steel, lumber, and concrete now cost significantly more than in previous periods, which directly elevates the replacement value of insured structures. Insurers adjust premiums to reflect these higher potential payouts in the event of damage or loss.

For instance, a standard builders risk policy now accounts for materials that may have doubled in price since 2020. This adjustment ensures coverage aligns with current market realities. Contractors who fail to update their policy limits face underinsurance risks, leading to out-of-pocket expenses during claims.

Heightened Climate Vulnerabilities

Extreme weather events have become more frequent and severe, prompting insurers to reassess risks in construction zones. Floods, wildfires, and storms pose greater threats to ongoing projects and completed builds, particularly in vulnerable regions. Data from recent years shows a marked uptick in claims related to these events, pushing premiums upward to cover anticipated losses.

Geographic factors play a crucial role here. Projects in coastal or wildfire-prone areas encounter even steeper hikes, sometimes exceeding the national average. Insurers employ advanced modeling to predict these risks, resulting in tailored rates that reflect localized dangers.

Stricter Regulatory Requirements

Governments and industry bodies have introduced tougher safety and environmental standards, which influence insurance underwriting. Compliance with new building codes demands additional safeguards, such as enhanced structural reinforcements or eco-friendly materials. These requirements increase project costs and, consequently, the liability exposure for insurers.

Moreover, regulations around worker safety and environmental impact have tightened, leading to more comprehensive coverage mandates. Policies now often include clauses for regulatory fines or delays caused by non-compliance. This evolution ensures broader protection but at a higher premium cost.

Impacts on Builders and Homeowners

Builders face immediate challenges as higher premiums strain project budgets. Margins shrink when insurance costs rise unexpectedly, potentially delaying timelines or reducing bids on future jobs. Small firms, in particular, struggle to absorb these expenses without passing them onto clients.

Homeowners undertaking additions or repairs encounter similar hurdles. Renovation insurance, often bundled with general liability, sees proportional increases. This can deter necessary upgrades, especially for those on fixed incomes who must balance protection with affordability.

Both groups must navigate more complex policy structures. Coverage exclusions for certain risks, like unpermitted work, have become more common. Clear documentation and adherence to guidelines help avoid claim denials.

Strategies to Manage Rising Premiums

Implement Robust Safety Protocols

Prioritizing safety reduces the likelihood of incidents, which in turn lowers insurance rates over time. Regular training for workers on hazard recognition and equipment use minimizes accidents. Insurers often offer discounts for projects certified under recognized safety programs.

Site-specific measures, such as secure fencing and weather monitoring, further demonstrate risk awareness. Documenting these efforts provides evidence during underwriting reviews. Consistent application yields measurable premium reductions.

- Conduct daily safety briefings.

- Invest in quality protective gear.

- Perform routine equipment inspections.

Optimize Project Planning

Detailed planning from the outset helps control costs and align with insurer expectations. Accurate risk assessments during the bidding phase identify potential vulnerabilities early. Selecting materials with lower volatility in pricing stabilizes overall expenses.

Collaborating with experienced brokers ensures policies match project needs without excess coverage. Bundling multiple policies, like general liability and workers compensation, can secure volume discounts. Reviewing terms annually keeps coverage current.

Homeowners benefit from phased approaches to renovations, spreading insurance needs over time. Consulting professionals for code-compliant designs avoids costly revisions later.

Enhance Communication with Stakeholders

Transparent dialogue with insurers, subcontractors, and clients builds trust and facilitates better terms. Sharing project timelines and risk mitigation plans upfront can influence underwriting decisions favorably. Prompt reporting of changes, such as scope expansions, prevents coverage gaps.

For homeowners, discussing needs with agents reveals options like higher deductibles to offset premiums. Educating family members on policy details ensures smooth claims processes. This proactive stance turns potential challenges into opportunities for stronger partnerships.

Building Resilience in an Uncertain Landscape

Adapting to the 45% premium surge requires a forward-thinking mindset. By addressing the root causes—material inflation, climate threats, and regulatory demands—industry participants can safeguard their operations. Practical steps like safety enhancements and precise planning deliver tangible benefits.

Ultimately, these efforts not only manage costs but also elevate project quality and reliability. Builders gain competitive edges through demonstrated responsibility. Homeowners secure lasting value in their properties. In this dynamic environment, resilience translates to sustained success and peace of mind.