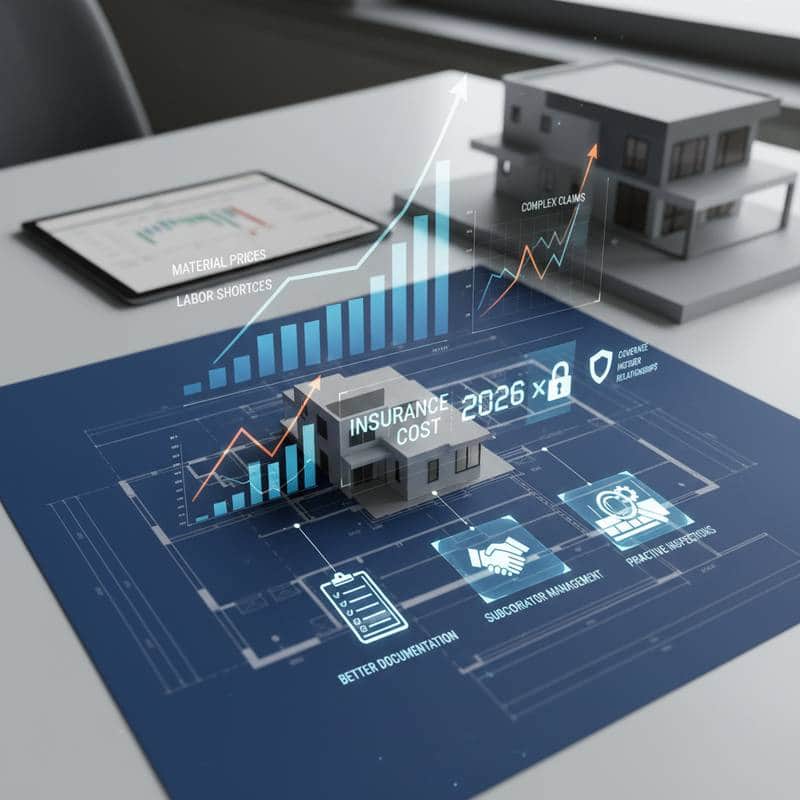

Prepare for Rising Construction Insurance Costs in 2025

Professionals in the construction industry often discuss the parallels between project planning and everyday routines. Builders review blueprints, lay foundations, and make adjustments as challenges arise. Recently, conversations among contractors, builders, and homeowners have centered on a pressing issue: insurance premiums. Projections indicate that construction insurance rates may triple by 2025, transforming this once-routine expense into a major factor in project viability.

For those involved in building, renovating, or overseeing construction, these changes demand attention. Previously, insurance served as a straightforward annual obligation. Today, it influences every stage of planning and execution. Understanding the drivers behind this increase and implementing adaptive measures will help safeguard projects and financial stability.

Drivers Behind the Projected Rate Increases

Several factors contribute to the anticipated surge in construction insurance premiums. Rising material costs, influenced by supply chain disruptions and inflation, elevate the value of assets at risk. Climate-related events, such as extreme weather, heighten the potential for claims related to property damage and delays.

Stricter underwriting standards from insurers further amplify these pressures. Providers now require detailed risk assessments, including site-specific evaluations and historical claim data. This shift reflects a broader industry response to escalating uncertainties, compelling builders to integrate insurance considerations early in the planning process.

To navigate this landscape, conduct a thorough risk audit before starting any project. Identify vulnerabilities, such as exposure to weather or material shortages, and quantify their potential impact on premiums. This proactive step allows for targeted adjustments that mitigate costs without compromising coverage.

Impacts on Builders and Project Budgets

A threefold increase in insurance rates can significantly alter financial projections for construction projects. For a typical mid-sized renovation, this jump might erode profit margins by 10 to 15 percent, depending on the scope. Developers and contractors face the challenge of reallocating funds or scaling back ambitions to accommodate these expenses.

Smaller operators should prioritize projects with lower risk profiles, such as interior work in stable urban areas. Medium-sized firms can benefit from negotiating group policies that distribute costs among multiple participants. Larger enterprises might implement layered coverage, combining general liability with specialized endorsements for high-value assets.

Active management proves essential in this environment. Review policies quarterly to align coverage with evolving project needs. Engage with brokers who specialize in construction to explore discounts for safety certifications or loss prevention programs.

Exploring Alternatives to Traditional Coverage

As premiums rise, builders seek innovative ways to manage risks without overextending budgets. Cooperative insurance groups enable members to share resources and negotiate better terms collectively. These arrangements often result in premiums 20 to 30 percent lower than individual policies, provided participants maintain high safety standards.

Self-insurance emerges as an option for financially robust firms handling predictable risks, such as minor equipment damage. Establish dedicated reserves based on actuarial projections to cover these exposures. Digital platforms now facilitate direct connections with specialized insurers, offering real-time quotes and customizable plans.

Before adopting any alternative, perform due diligence. Assess the financial stability of group members or platform providers. Consult legal experts to ensure compliance with regulatory requirements, avoiding unintended liabilities.

Considerations for Homeowners and Owner-Builders

Homeowners undertaking renovations or new constructions encounter these rate hikes indirectly through builder quotes. Premiums embedded in contracts can inflate overall expenses by five to ten percent. Owner-builders, who manage projects personally, must secure coverage independently, amplifying the need for informed decisions.

Builder's risk insurance typically protects against physical damage to structures during construction. Separate policies address liability for worker injuries or third-party claims. Request itemized breakdowns from builders or brokers to identify gaps in protection.

Minimize risks through meticulous documentation. Maintain logs of material purchases, site progress, and safety measures. This practice not only streamlines claims but also demonstrates risk awareness to insurers, potentially qualifying for premium reductions.

Building Resilience Through Proactive Habits

Adopting consistent practices strengthens defenses against rising costs. Schedule comprehensive insurance reviews annually, ideally during off-peak seasons, to allow time for adjustments. Foster collaboration among accountants, brokers, and project managers to ensure seamless integration of financial and operational insights.

Document all safety enhancements, from equipment upgrades to training programs, and submit them to insurers as proof of proactive risk management. Train site teams on policy details, clarifying roles in incident reporting and prevention. These measures convert insurance from a mere expense into a strategic asset.

Strengthening Projects Against Insurance Challenges

By addressing these evolving dynamics head-on, builders and homeowners position themselves for sustained success. Early integration of risk strategies preserves budgets and timelines. This approach not only protects assets but also enhances overall project confidence and profitability.