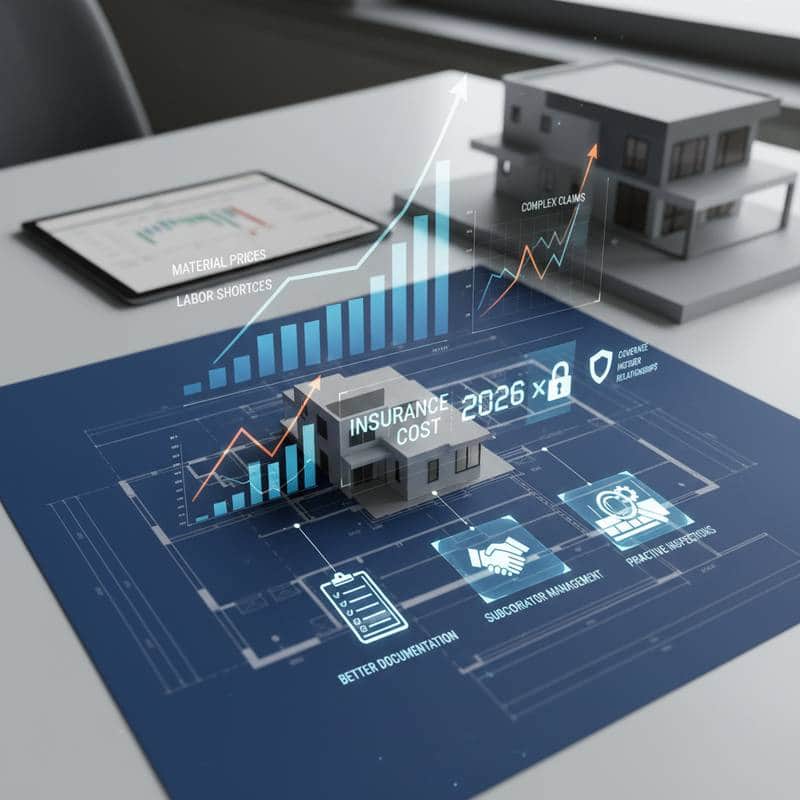

Why Construction Insurance Costs Surged 85 Percent in 2025

Picture completing a home addition after months of dust and noise, only to discover that the builder's insurance premium has nearly doubled. This sharp increase in construction insurance costs has surprised many. Builders, subcontractors, and homeowners planning renovations now face a significant expense that demands attention. The following sections explain the causes and outline practical responses.

Understanding Builder Liability Insurance

Builder liability insurance once provided simple protection against on-site injuries, property damage, and defects. Today, policies include multiple exclusions and elevated deductibles. Insurers require comprehensive risk management plans, regular safety audits, and evidence of subcontractor training programs.

For small builders, these demands can consume substantial time. Consider a three-person carpentry operation where renewal documentation exceeds the effort needed to frame a modest deck. This scrutiny represents the current industry standard. Insurers seek proof that builders address risks in advance rather than after incidents occur.

Underwriters monitor regional patterns with precision. Areas prone to high humidity or unstable soil experience elevated defect claims. Urban settings present greater liability risks from confined work areas. Projects in such locations typically incur higher premiums as a result.

Key Factors Driving the Premium Increase

Multiple interconnected elements contribute to the 85 percent rise in premiums:

- Material Cost Inflation: Elevated prices for replacements lead to larger claim settlements. Increases in lumber and steel costs establish a higher threshold for all repairs.

- Labor Shortages: A reduced pool of skilled workers results in more frequent errors. This pattern elevates the overall number of claims.

- Regulatory Demands: Stricter safety and environmental rules impose additional expenses on both insurers and builders.

- Severe Weather Events: Extreme conditions now impact more projects, causing water intrusion, project delays, and structural damage.

- Rising Litigation: Disputes have increased in volume and intricacy. Even minor conflicts often resolve with settlements in the five-figure range.

These factors compound one another, forming what insurers describe as a hard market. This environment features limited insurer participation in construction risks and elevated pricing from those remaining active.

Leveraging Local Suppliers and Brokers

Engaging regional partners offers a way to offset cost pressures. Local brokers possess knowledge of competitive insurers in specific areas and maintain connections unavailable to national entities.

Material suppliers play a vital role as well. Providers that offer quality certifications or their own liability protections can diminish overall exposure. For example, certain regional paint manufacturers provide warranties against adhesion issues, which has helped reduce defect risk assessments.

Inquire with suppliers about certificates of compliance and material traceability records. These items serve purposes beyond regulatory inspections. They demonstrate to insurers a commitment to rigorous quality control.

Implementing Effective Strategies

The rise in construction insurance costs presents challenges, yet viable coverage remains accessible. Markets adjust over time, and proactive builders typically achieve better outcomes. View insurance as an integral business component rather than an obstacle.

Build insurer confidence similarly to client relationships. Each successful inspection, efficiently managed project, and recorded safety protocol enhances professional standing.

Upon completing the most recent project, satisfaction extended beyond the quality of work to the security provided by reliable coverage. Such assurance holds particular value in uncertain times.